Understanding Sep 25th’s BTC Price Volatility with On-Chain Data

After the recent drop in price, using our on-chain data, the research team at CryptoQuant looked for a potential cause. Although we didn’t find a cause for the most recent price movement, we found a correlation between the BitMEX withdrawal system and the timing of big price movements

Using Outflow for Anticipating Short Term BTC Price Changes

Using our on-chain data, investors can look into BitMEX outflows as a leading indicator for mass liquidations and the large volatility that results. It is then possible to more successfully hedge against this risk. BitMEX, as the most liquid BTC exchange and the largest physically settled futures exchange, exerts a large impact on price. It is well understood that the effect of margin calls, specifically cascading margin calls on BitMEX, can cause large swings in price much like yesterdays. But a more in-depth look is required.

BitMEX Futures and Outflow as Predictor of Low Liquidity

Flow models have been consistently used as a metric for understanding price. Here inflows and outflows of BTC and stable coins can be interpreted to have specific implications on price. Analysis regarding this is well established, but standard models of Inflow/Outflow aren’t compatible with BitMEX. Traditional exchanges trade between BTC and fiat. This is why Inflow/Outflow metrics are used as indicators in order to understand market structure. For example, when large amounts of BTC are withdrawn from an exchange, it can be viewed as an increase in the amount of HODLERs, drying up supply, and pushing price up.

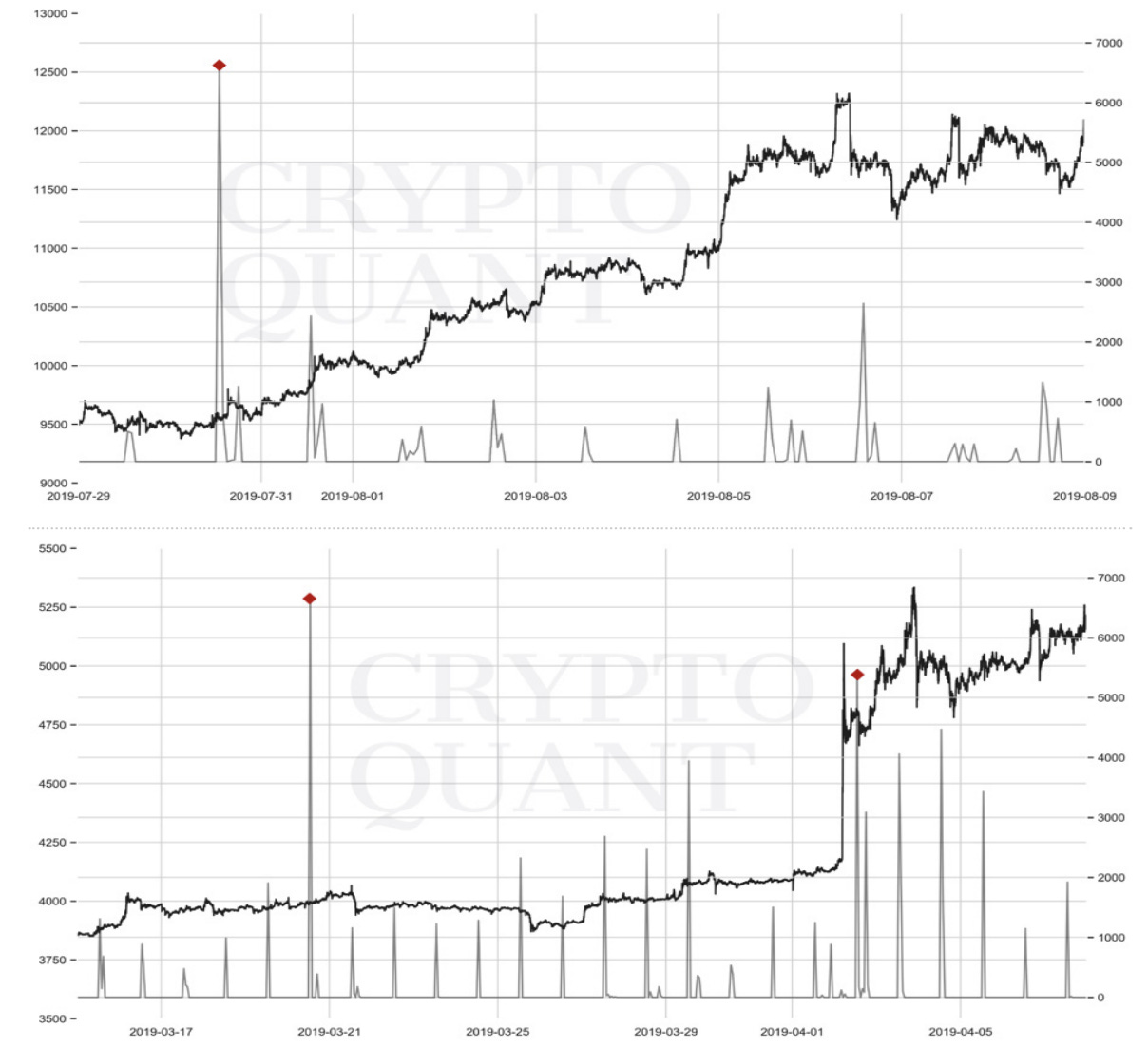

During these three periods (2018.11.15 ~2018.11.21, 2019.03.17~2019.0 4.05,2019.07.17~2019.07.19, 2019.07.29~2019.08.09) during which BTC experienced a similar change in price, BitMEX Outflow has been overlaid onto the graph. The large Outflow that takes place immediately prior to high volatility is clearly illustrated. Source: CryptoQuant

Conversely, BitMEX BTC outflows have a large impact on volatility, but this can lead price to increase as well as decrease. This is a result of BitMEX’s unique withdrawal policy. Deposits are constantly available, but withdrawals are only conducted once daily, at UTC 13:00. During this short period, outflows exceed inflows by large multiples. Immediately following this, a liquidity shortage, and an increase in the spread can often be observed. These properties lead BitMEX margin positions to be exposed to a liquidity shortage and cascading liquidations. This idea is supported by the BitMEX wallet Outflow data pulled from on-chain. Using this data, it is possible to anticipate these large volatility moves caused by BitMEX withdrawals. When the Outflow on BitMEX exceeds a certain point, the potential for these large moves increases significantly. Based on on-chain data, it currently appears that when more than 5,000 BTC are withdrawn in one day, the exposure to this volatility increases significantly. Looking at our on-chain data regarding inflows and outflows from BitMEX on 18.11.14, and 19.04.02, we can see that there is a clear correlation price volatility and outflows. On each of these dates, the volatility occurred within a short period following the BitMEX daily withdrawal at 13:00 UTC. Once the ability of the market to absorb small changes in price decreases, price quickly responds, moving in one direction or another.

For example, looking at the outflows on 18.11.14, we can see that price moved within a few hours of the UTC 13:00 mark. Within 3 hours it had fallen 11% and a total of 15.6% after 8 hours. Because of the precision of the on-chain data, we can see the exact block in which the BitMEX outflows spiked. Without consistent and precise on-chain data, on-chain metrics like outflow lose their utility and become lagging instead of leading indicators. The shortness of the window here cannot be overemphasized.

BitMEX Margin and the Premium Establishing Directional Bias

Although Outflow allows us to obtain an understanding of incoming volatility, it falls short of providing insight into the direction which this volatility will lead. For this, the BitMEX Funding and Premium Index provided by NeoButane proves to be useful in gauging whether longs or shorts are overly margined, and thus more vulnerable to the incoming liquidity risk. Again referring to 19–04–01, the premium was in favor of shorts, with longs paying the funding fee. Price responded as the indicators anticipated, and fell as longs were exposed to the liquidity risk and cascading liquidations ensued.

Further Research

During our research into BitMEX’s withdrawal system, we also noticed a record large internal movement of BTC on 19.09.24. During one hour, nearly 100,00 BTC was moved between BitMEX wallets. Although we don’t believe this would have a direct on price, it is worth looking more into. We will provide analysis regarding this in a future report.

Conclusion

Currently most on-chain data is used for long term metrics. These include NVT and MVRV as developed by Willy Woo and Adaptive Capital. Their and others work has shown the significance of on-chain analytics for long term positions. BitMEX Outflow is somewhat unique in that it is a short term onchain metric. It enables traders to quickly identify a coming liquidity crisis and hedge accordingly. This expanding use of on-chain data furthers the ever-growing importance of on chain data in building a winning strategy when operating in BTC markets.

SUBSCRIBE TO OUR REPORT